In my previous blog post I looked at what accounts can be added to the system and the benefits of adding things like loyalty programmes and assets. In this blog post I will be looking at what 22Seven tells you out the box. In other words, using the standard categories and reports, what can we learn about our finances?

Categories

22Seven has categorised transactions rather cleverly. Not only do transactions go into categories like ‘car expenses’ and ‘groceries’, but they are also further categorised into high level categories of ‘day to day’, ‘recurring’ and ‘exception’, etc. These are fixed categories. We will see later why these are very useful.

I’ve realised that correct categorisation is the key to getting the most out of 22Seven. Which means you need to do a little thinking upfront. The built in categories, while they cover quite a few things (there are about 40 of them!), might not quite suit the info you are wanting to get out of it. For instance, you car might be a big expense for you so you may want to analyse you car expenses in more detail. There are categories for ‘car repayments’, ‘transport & fuel’ and ‘car expenses’. Those are a good basic starting point, but I have actually created a category specifically for ‘fuel’, which means I can see at a glance what my fuel expense for the month is, something I can reduce if I am going over budget but simply being careful about the amount of driving I do. Transport for me covers my Uber/Taxi rides, my MyCiti bus card, etc. Also a useful set of expenses to monitor.

Another item which may want more attention is entertainment. For many people this is a big element of their budget so you might want to break it down more specifically. There are built-in categories for ‘Eating out & Take-aways’ and ‘Entertainment’, but those are quite broad. I would create a category for ‘Restaurants’, ‘fast food’ and ‘bars’. This means I can see straight away where my money is going and I can budget at a more granular level, so perhaps only allow myself to go to a bar once a week.

Once you have set up your categories, you need to glance over your transactions in each of your accounts to check that you are happy with the allocation. 22Seven will auto-allocate transactions for you but it doesn’t always get it right, especially if you have added your own categories. It’s quite easy to select the account and run your eye down the list of transactions and their allocation. Simply click the transaction to edit it if you want to change the category.

Reporting

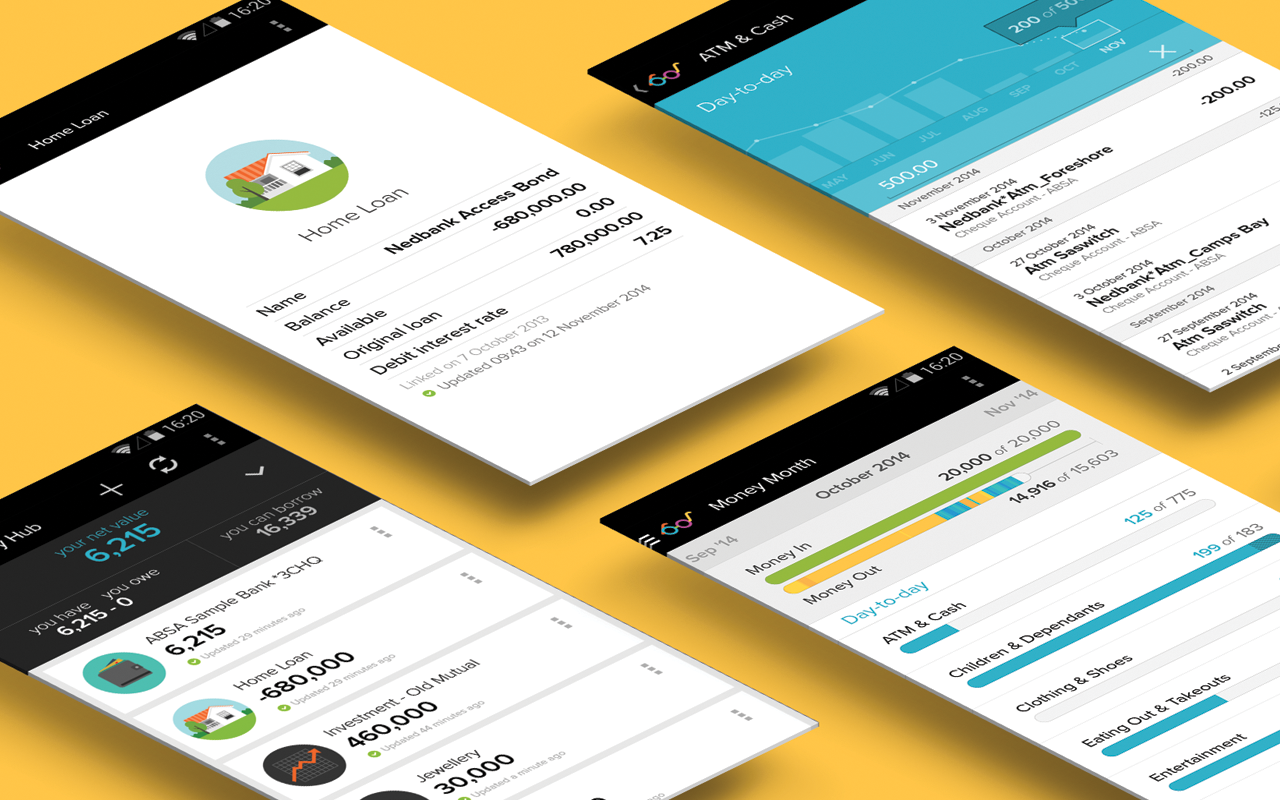

The main report in the system is the ‘Money Month’. This shows you for the current month how your spending is going per category. It shows you your spending relative to your average spending over the last 3 months for that category, or your budgeted (planned) expenditure for that category. This is really powerful because you can see straight away for instance, it’s only the middle of the month and I’ve spent R2,000 at restaurants but I usually spend R2,000 in a full month so I need to be careful for the rest of the month with eating out.

The ‘Track’ view shows you your categories sorted by high level category. So for instance, you might have a bunch of car expenses this month, some of them are categorised as ‘day to day’, like car wash, parking, etc. Others can be categorised as ‘exceptions’ eg, service or parking tickets. This shows you your expenditure according to a normal month, and you can see separately the additional once off things you’ve had to fork out for this month as well. This is what makes the high level categories so important.

When you switch to the ‘Compare’ mode, your Money Month report shows you all your income and expenses in order of size so you can see which categories are your big spenders. Don’t just look to the big categories for savings, those little categories can add up too. Like bank charges, those can be reduced if you put in a little effort. And if you can reduce a few of your smaller categories by 20%, it will make a big difference to your budget.

One of the things which bugged me was that you can’t change the date of transactions. I understand why they don’t allow you to, but seeing as it’s my tool to manage my finances I would like to be able to change some dates in order to put expenditure in the correct place. For instance, sometimes my car insurance comes off on the last day of the month, other times it’s the first day of the next month. So some months I have no car insurance expenditure and other months I have double. There are a bunch more reasons why I would want to change transaction dates, which I won’t bore you with but I really hope this feature is included soon.

What did I learn?

Because the Money Month report shows me my average spend per category for the last 3 months, I can see at a glance how much I am spending on each category. By creating my own categories I can make it so that I can see the average at quite a granular level. This gives me an indication of where my money is going, and therefore where I could potentially save money.

Having my transactions broken down into ‘day to day’, ‘recurring’ and ‘exceptions’ showed me how much of my expenditure I can actually change. Recurring transactions include things like rent, car repayments, etc. These are fixed so I can focus on the other transactions where I can actually make changes and I’m able to see the impact it will have on my budget.

In my last article I will be looking at the transaction filter and what we can learn by using that powerful tool, as well as some advanced techniques for getting the most out of it.

If you want to join me on this adventure, download the app (Android or iOS) and if you’re keen to share your feedback on your experience, leave comments on my posts

This is a sponsored post.